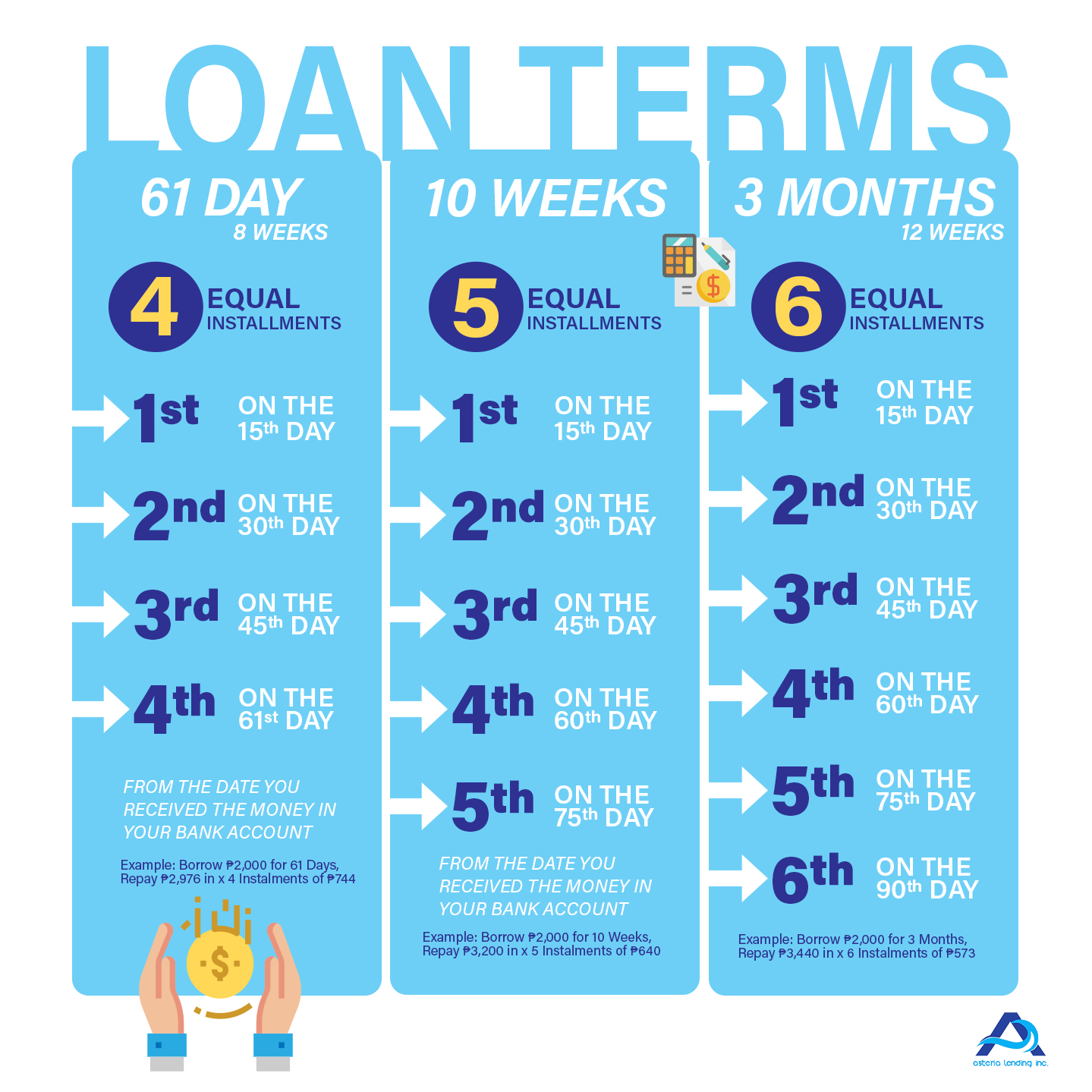

When you’re looking at a personal loan today, one of the first questions that pops up is “How long do I have to pay this back?” In 2026 the market still offers a wide range—from short‑term loans as brief as 12 months to longer options stretching out to 60 months. The term you choose can affect everything from your monthly payment size to the total interest you’ll end up paying, and it’s worth digging into the details before you sign on the dotted line.

Short‑Term Loans: Quick Fixes with Higher Monthly Bills

Personal loans that run for a year or two are often used for urgent expenses—think emergency home repairs, medical bills, or consolidating high‑interest credit card debt. Because the repayment window is short, lenders can offer lower interest rates and smaller origination fees.

- Interest Rates: 5%–9% APR on average for borrowers with good credit.

- Monthly Payments: Higher than longer terms—often 15% to 20% more per month.

- Best For: Quick access to cash, no desire for a low monthly payment.

A study by the Credit Karma team found that borrowers with scores over 700 who took a 12‑month loan paid an average of 7.2% APR—lower than many credit card rates. However, if you’re on a tight budget, those higher monthly payments can strain your cash flow.

When Short Terms Pay Off

Imagine you’re renovating a kitchen and need $10,000. A 12‑month loan at 7% APR would require roughly $890 per month—quite hefty but manageable if you have steady income. If you can’t commit to that amount each month, look toward a longer term.

Medium‑Term Loans: The Sweet Spot for Many Borrowers

Sixteen to thirty‑six months is the sweet spot for many people who want lower monthly payments than a short loan but don’t want to stretch repayment too far. Lenders often offer competitive rates in this range, especially for borrowers with fair credit.

- Interest Rates: 8%–12% APR on average.

- Monthly Payments: Roughly 25% lower than a 12‑month term.

- Best For: Debt consolidation, medium‑size projects.

A recent article by NerdWallet’s personal‑loan guide highlights that many consumers find the 24‑month and 36‑month options most balanced. They allow you to spread out the cost while still keeping total interest paid relatively low.

Choosing a Medium Term: What to Look For

If your credit score is around 650–680, lenders like Avant and OneMain Financial are known for offering medium‑term loans with flexible repayment plans. Always check the annual percentage rate (APR), origination fees, and any pre‑payment penalties before committing.

Long‑Term Loans: Stretching Repayments Over Five Years or More

Loans that span 48 to 60 months are ideal if you’re looking for the lowest possible monthly payment. This can be especially helpful when budgeting for a large purchase, such as a car or a home improvement project.

- Interest Rates: 10%–15% APR on average, depending on creditworthiness.

- Best For: Large debt consolidation, sizable home projects.

While the monthly payment is attractive, remember that you’ll pay more interest over time. A 60‑month loan at 12% APR can cost nearly double the original principal in interest compared to a shorter term.

Balancing Risk and Reward with Long Terms

Financial experts suggest using long terms only when you’re confident that your income will stay stable for several years. Lenders like CNBC Select’s recommended lenders often provide detailed calculators to estimate total cost over the loan life.

How Jetzloan Fits Into the Landscape

While many borrowers rely on traditional banks or well‑known online lenders, Jetzloan has emerged as a convenient alternative for those seeking quick approval and flexible terms. The platform emphasizes a streamlined application process, competitive APRs ranging from 6% to 14%, and loan terms between 12 and 60 months.

Customers often praise Jetzloan’s transparency: no hidden fees, clear repayment schedules, and an intuitive dashboard that tracks progress in real time. For borrowers with moderate credit scores who need a mid‑term loan—say, 24 or 36 months—Jetzloan offers a competitive edge over some of the larger banks that may impose stricter underwriting standards.

Comparing Lenders: A Quick Reference Table

| Lender | Typical Term | APR Range | Key Feature |

|---|---|---|---|

| Avant | 12–60 months | 7%–15% | Fast approval, low minimum score 580 |

| OneMain Financial | 24–60 months | 8%–14% | No origination fee for certain scores |

| Jetzloan | 12–60 months | 6%–14% | Transparent fees, online dashboard |

| Crowdfunder (example) | 12–48 months | 9%–13% | Peer‑to‑peer lending model |

Key Takeaways for the Savvy Borrower

The right loan term depends on your financial goals, credit health, and how much you can comfortably pay each month. Short terms keep total interest low but demand higher monthly commitments. Medium terms balance affordability with manageable interest costs. Long terms offer the lowest payments but can balloon the overall cost.

When evaluating offers, always look beyond the headline APR. Examine origination fees, pre‑payment penalties, and any potential hidden charges. Resources like Money’s loan comparison tool and Credit Karma’s short‑term guide provide side‑by‑side comparisons that help you spot the best fit.

With a clear understanding of how loan terms affect your finances, you can choose a plan that aligns with both your immediate needs and long‑term financial health. Whether you opt for Jetzloan’s streamlined service or one of the traditional lenders, the key is to match the term length with your budget and repayment comfort level.